Net Present Value (NPV) is a fundamental concept in finance, a powerful tool used for capital budgeting and investment analysis. In essence, NPV calculates the present value of expected future cash flows from an investment or project, discounted by a required rate of return, and then subtracts the initial investment cost. The resulting figure indicates whether the investment is expected to generate a positive return above the cost of capital.

The core principle behind NPV rests on the time value of money. A dollar today is worth more than a dollar received in the future because of its potential earning capacity. This earning capacity stems from the ability to invest the dollar and earn a return over time. The discount rate used in the NPV calculation reflects this opportunity cost – it represents the return that could be earned on alternative investments of similar risk.

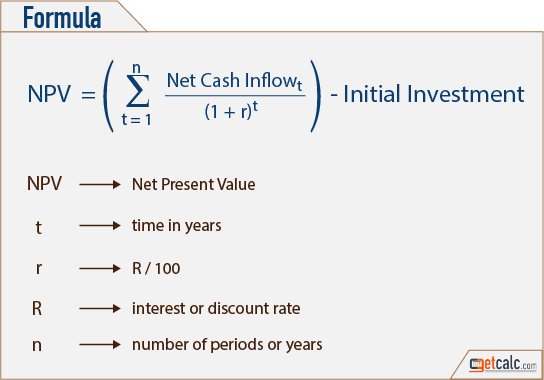

The formula for calculating NPV is as follows:

NPV = Σ [CFt / (1 + r)t] – Initial Investment

Where:

- CFt = Cash flow in period t

- r = Discount rate (required rate of return)

- t = Time period

- Σ = Summation (sum of all cash flows)

The process involves several key steps. First, you must estimate all future cash inflows (revenues) and cash outflows (expenses) associated with the investment over its entire lifespan. This requires careful forecasting and consideration of various factors like market conditions, operating costs, and potential obsolescence. Second, you need to determine an appropriate discount rate. This is often the weighted average cost of capital (WACC) for the company or a rate that reflects the riskiness of the specific investment. Higher risk projects warrant higher discount rates. Finally, you plug these values into the NPV formula and calculate the present value of each cash flow. Summing these present values and subtracting the initial investment gives you the NPV.

The interpretation of the NPV is straightforward:

- NPV > 0: The investment is expected to generate a positive return exceeding the required rate of return. The project is considered acceptable and should increase the value of the firm.

- NPV = 0: The investment is expected to generate a return equal to the required rate of return. The project breaks even and has no impact on the value of the firm. While not actively harmful, it may not be the best use of resources.

- NPV < 0: The investment is expected to generate a return less than the required rate of return. The project is considered unacceptable and would decrease the value of the firm.

NPV offers several advantages. It considers all cash flows over the project’s life, accounts for the time value of money, and provides a clear decision rule. However, it also has limitations. Accurately forecasting future cash flows can be challenging, and the choice of discount rate significantly impacts the result. Moreover, NPV alone doesn’t consider the scale of the investment. A project with a higher NPV may require a substantially larger initial investment compared to a project with a slightly lower NPV but a smaller upfront cost. Therefore, NPV is best used in conjunction with other financial metrics and careful qualitative analysis to make informed investment decisions.

960×720 net present npv definition from gbu-taganskij.ru

960×720 net present npv definition from gbu-taganskij.ru  1024×512 npv definition formulas advantages disadvantages from exceldatapro.com

1024×512 npv definition formulas advantages disadvantages from exceldatapro.com  1024×576 net present npv definition examples npv from www.yakimankagbu.ru

1024×576 net present npv definition examples npv from www.yakimankagbu.ru  1872×1112 npv profile corporate finance cfa level analystprep from analystprep.com

1872×1112 npv profile corporate finance cfa level analystprep from analystprep.com  953×319 net present npv definition parsadi from parsadi.com

953×319 net present npv definition parsadi from parsadi.com  343×157 net present npv definition calculation examples from xplaind.com

343×157 net present npv definition calculation examples from xplaind.com  1408×497 net present npv mission control from aprika.com

1408×497 net present npv mission control from aprika.com  571×486 net present npv profile definition explanation from www.accountingformanagement.org

571×486 net present npv profile definition explanation from www.accountingformanagement.org  1200×1698 definitions definition npv irr define net present npv from www.studocu.com

1200×1698 definitions definition npv irr define net present npv from www.studocu.com  544×380 net present npv definition formula images from www.aiophotoz.com

544×380 net present npv definition formula images from www.aiophotoz.com  1500×1093 acronym npv net present stock illustration shutterstock from www.shutterstock.com

1500×1093 acronym npv net present stock illustration shutterstock from www.shutterstock.com :max_bytes(150000):strip_icc()/npv-rule.asp-final-b5079630617a4938af59f6ace6e287f6.png) 1500×1013 net present npv rule definition from www.investopedia.com

1500×1013 net present npv rule definition from www.investopedia.com  1500×1150 npv net present acronym business stock vector royalty from www.shutterstock.com

1500×1150 npv net present acronym business stock vector royalty from www.shutterstock.com  1024×768 npv from studylib.net

1024×768 npv from studylib.net  1024×397 npv net present definition benefits formula examples from www.hashmicro.com

1024×397 npv net present definition benefits formula examples from www.hashmicro.com :max_bytes(150000):strip_icc()/NPV-bfe8422ba272436cae4e1b5138fd306b.JPG) 818×645 net present npv means steps calculate from www.investopedia.com

818×645 net present npv means steps calculate from www.investopedia.com  1024×768 npv irr capital budgeting powerpoint id from www.slideserve.com

1024×768 npv irr capital budgeting powerpoint id from www.slideserve.com  601×601 net present npv explained definitions formula examples from www.capitalcitytraining.com

601×601 net present npv explained definitions formula examples from www.capitalcitytraining.com  550×543 net present npv definition formula from theinvestorsbook.com

550×543 net present npv definition formula from theinvestorsbook.com  1200×650 npv formula works private capital investors from privatecapitalinvestors.com

1200×650 npv formula works private capital investors from privatecapitalinvestors.com  181×233 understanding npv capital structure corporate finance hero from www.coursehero.com

181×233 understanding npv capital structure corporate finance hero from www.coursehero.com  1000×375 npv net present cash flows required rate return from stock.adobe.com

1000×375 npv net present cash flows required rate return from stock.adobe.com  800×400 importance npv financial model oak business consultant from oakbusinessconsultant.com

800×400 importance npv financial model oak business consultant from oakbusinessconsultant.com  1600×1290 npv net present acronym stock illustration illustration from www.dreamstime.com

1600×1290 npv net present acronym stock illustration illustration from www.dreamstime.com  1792×860 npv work phoenix partners chartered surveyor from phoenixandpartners.co.uk

1792×860 npv work phoenix partners chartered surveyor from phoenixandpartners.co.uk  1024×526 images npv japaneseclassjp from japaneseclass.jp

1024×526 images npv japaneseclassjp from japaneseclass.jp